Share as you like for non-profit use, but please be sure to identify Dave as the author and include the website address

Share as you like for non-profit use, but please be sure to identify Dave as the author and include the website address

Global Financial Meltdown: Forces beyond our control? Or the biggest Sting ever?

Global Financial Meltdown: Forces beyond our control? Or the biggest Sting ever?

by

Dave Patterson

March 2009

To listen to the news these days, with its endless stories of yet more tragedies amongst 'we the people', you would think it was all just some inevitable unfolding of history, some kind of natural disaster that happens every now and then that we can do nothing about, but just have to grit our teeth and get through it, like the big ice storm a few years ago, or the recent tsunami that took so many lives around the coastal areas of the Indian Ocean, or the hurricanes that regularly strike around the Gulf of Mexico, and etc. Every day we hear on the news more stories of the latest victims, and how our noble governments are trying their very best to steer our ships of state through these troubled waters.

Like so much of what we hear on the news, this is all one step short of what is really going on in our lives, in the world around us. The stories of human tragedies amongst we the little people are true enough - but what they are lying about is the 'natural disaster' aspect of it all. These tragedies we read of, the job losses, the loss of huge amounts of money and property by 'average' citizens, need not have happened at all. What we are really seeing is the biggest sting ever perpetrated in history, conducted by the elite who control our society, using the vehicles of the banks and governments and media they control to feed us all the basic sting story of unforeseen, unforeseeable, unprecedented natural disaster, whilst behind the scenes and even brazenly in the open in front of our mesmerized eyes transferring vast amounts of the wealth produced by the working people of the world into their own private coffers in the name of dealing with this 'disaster', and using the fear and uncertainty to impose debts that our children and their children will be paying off, to these same scamsters, for decades to come.

As with any sting, there are many marks and few scamsters, and we could stop them if we just stood up together and said we are not going to allow this theft. We are going to take the lot of you, put you on public trial for vast fraud, take our money and countries back, and send you all to jail for the rest of your lives.

We could. The question is, will we? If most of us continue to sit in front of the televisions and believe the sting 'terrible tragedy nobody could have seen it coming!!' stories they feed us every day, it is unlikely that any uprising will occur - what can you do about a 'natural unpreventable disaster' except do your share, shoulder to shoulder, to stand strongly against the forces of nature, and rebuild our society together? But if you turn off the television, and turn on your brain, and realise what a huge scam this whole thing really is, and the brazen theft of not only your money but the money of your children and grandchildren who will be paying these fraudulent debts for generations - then maybe you will find the strength and wisdom to do what is really necessary - stand up and say No More!!! - take control of your democracy, take back your money from those who are stealing it in front of your very faces, and send all of them to jail for the rest of their lives.

We could. The question is, will we? If most of us continue to sit in front of the televisions and believe the sting 'terrible tragedy nobody could have seen it coming!!' stories they feed us every day, it is unlikely that any uprising will occur - what can you do about a 'natural unpreventable disaster' except do your share, shoulder to shoulder, to stand strongly against the forces of nature, and rebuild our society together? But if you turn off the television, and turn on your brain, and realise what a huge scam this whole thing really is, and the brazen theft of not only your money but the money of your children and grandchildren who will be paying these fraudulent debts for generations - then maybe you will find the strength and wisdom to do what is really necessary - stand up and say No More!!! - take control of your democracy, take back your money from those who are stealing it in front of your very faces, and send all of them to jail for the rest of their lives.

Manic Depressive People Can Be Helped - So Can Manic Depressive Economies

Our 'modern' economy has all the symptoms of someone with manic-depressive disorder, bouncing between periods of great exuberance followed by periods of depression. This is somewhat misleadingly referred to by our 'experts' (economists, financial leaders, business commentators, etc) who influence the policies under which our economy operates as the 'boom-bust business cycle', as if they are, with their great learning, pontificating some great Law of Nature that cannot be changed or challenged but only dealt with as best we all can when the regular cyclical disasters such as we are facing today fall upon us. But these modern priests of the god mammon speak falsely, whether from ignorance or perfidy, and such disasters need not occur at all. Think of automobiles - we could remove all road rules and policemen, and call the resulting carnage a 'law of nature' as people do what comes naturally - or we can choose to say that letting people do as they wish on our highways does not qualify as an immutable law of nature, and this carnage is not acceptable in a civilized society looking out for all of its citizens rather than letting the few crazies behave as they wish, and can be minimized, and do so.

And we could do the same with things economic, if we wanted to. We could choose sanity over insanity, a stable economy over a roller coaster casino economy that is great fun and very profitable for the few and highly precarious and periodically disastrous for the many, if 'we' (as in 'We the People') understood what was happening with our economy, and the choices available as to whether we allow this manic-depressive 'business' cycle to be the norm, or whether we choose to run our economy in a more stable way, to legislate the psychotic drivers who make life precarious for everyone off of our national financial highway. It is simply a matter of political will - however, unfortunately for most of us, currently the decisions that determine what happens in 'our' economy - the actual manifestations of 'political will' - are in the hands of a select group of people who prefer this manic-depressive cycle and thus ensure that our financial system and laws enable this 'business cycle' rather than control it, as they make a lot of money from it in either stage. Also, collectively, of course, the same people, as the ones with the money, pretty much manage the overall direction of our market-oriented 'everything for sale to the highest bidder, including politicians' society, with 'we the people', with far too little money to be purchasing the services of these highest of the high rollers, reduced to 'choosing' between Banker Bob and Lawyer Lois every few years then sitting back in front of our televisions to see what they are doing, with no real power to influence anything between 'elections'. The same people, via the same purchasing power, also control the media, and thus ensure we don't get any real information about what is going on with either the financial policies or the enabling political decisions, or other options that might jeopardize their power. With considerable success, it must be said, as few of 'we the people' seem to have any real idea of what is happening with our economy, or that we could do something about these destructive cycles, and don't take to the streets in protest at the great theft of our wealth engineered by the current policies, which are very much policies of choice rather than necessity, choices which are very good for the few, and very bad for the many.

But if you would like to see your society on a somewhat more even keel financially than this boom-bust-bubble roller coaster thing they pretend is some kind of law-of-nature 'business cycle', read on. If the sight of pension funds vanishing in the market maelstrom troubles you, or the hundreds of thousands of job losses we are seeing as the economy contracts, or the thought of the government going even deeper into debt, for which your children will surely be paying for decades to come if the status quo is not challenged, or you think there should be a better way to organise things than watching the price of oil and housing and the stock market and even your currency bouncing around like ping pong balls as the global speculators play unhindered in our societies, read on. There are indeed other ways to run our economy, other much more stable ways, than having Mad Uncle Milton, and Steve and Mark and Jim and the others in their gang, at the wheel.

If you want it, you can have it. But you'll have to demand it and then take it, for it is certain that the captains of the good ship Midas the Golden Goose surely won't surrender their positions without a serious struggle.

As Henry said, look for the root ...

As Henry said, look for the root ...

The first part of the struggle of We the People to gain control of our economy and lives comes with knowledge, knowledge of the way things work that the current economic overlords, and their enabling managers, have but we do not. Understanding the source of any problem is fundamental to fixing it. Bowing to the god Mammon and believing without question the pronouncements of its high priests is the path to continuing slavery - understanding their lies is the path to freedom. And the source of every major economic problem we face today (and have for the last couple of hundred years) is that most of our money - the money that is the lifeblood of a modern economy, that controls everything we do - is controlled and created as debt by commercial banks, with (currently) no realistic, government-controlled limits imposed on the amount created, and upon which they demand interest every year.1

Don't race on, this is not some esoteric factoid of theoretical interest only to egghead economists or quantum physicists, it is the single most important fact of all, the fact that, if understood, can open the door that will show the way to a new and sane economic regime for all of us, a fact that explains every problem we face today, and if you want to be part of the solution rather than just another of the millions of victims, you have to understand this fact, and what it means.

Let's then repeat it once again - 'our' government does not provide our money supply, nor even control how much is created. And all major problems we face in the world today arise from this single, simple fact.2

This is it, one simple fact, but a fact known by very few people which is the key to everything: commercial banks create virtually all of our 'money', out of thin air, as loans, simply by punching numbers into a computer.

The ramifications of this one simple fact are huge. So huge that the current world economic meltdown is a direct result of this simple fact. Every bubble that has burst over the last few decades, with huge loss of money, is the result of this one simple fact. The Canadian national debt, that has been used as the excuse for so many cutbacks to Canadian social programs, the lack of money that has led to crumbling infrastructure, the huge increases in post-secondary education expenses, the long waiting lines at hospitals, the declining savings and increased debt faced by all Canadians, all of these and every other economic problem we face, are due to this one simple fact - commercial banks create virtually all of the Canadian money supply as debt.

And this is a matter of policy which can be changed at will, not some kind of 'law of nature' that we can do nothing about.

A couple of related facts to help put this in perspective:

There is about $50 billion of 'real' Canadian money, bank notes and coins, in circulation, the money you are most familiar with, that you take from your pocket or wallet when you need to pay for your hamburger or some groceries or gas or movie tickets or rides at the fair or any of the millions of little transactions that occur every day in Canada between consumers and small businesses. But this is only the smallest amount of all the 'money' we use - there is also at least $3 Trillion of Canadian debt outstanding, business, consumer and government. Although the myth they want you to believe is that 'loans' are simply bank deposit money that banks lend out, you can see that it would be more than a bit difficult to arrange $3 Trillion in loans from $50 billion in deposits of this 'real money' by simply loaning out 'your' deposits that you or other depositors are not currently using - and even more so when you figure that most of that $50 Billion is not deposited in banks anyway, but circulating in the pockets of every Canadian citizen and business to conduct normal daily cash transactions, as well as good chunks of it floating around most countries in the world in money changers' shops etc. It is this $3 trillion in debt that comprises the great bulk of the Canadian money supply, that is shuffling around electronically between the millions of personal and business bank accounts every day, that I am talking about when I say commercial banks create almost all of our money supply, and that lies at the root of our current meltdown and other financial problems.3

It may not be immediately clear why this is such a problem. But think of it, just imagine this process and let it become clear in your head, for this is the first and major thing we need to understand and change if we want to establish a stable economy. Essentially, to create 98% of the nation's circulating electronic money supply, all that money changing hands every day via credit and debit cards and cheques, banks make loans to businesses, consumers or governments, creating that loaned money out of thin air. And then, when the loan is paid back, the money is 'uncreated' - and then they make other loans, which keep money available and circulating in the country, an endless, ongoing creation-uncreation process, like the ocean tides going in and out - with an equally never-ending demand for interest on the continually extinguished and re-birthed debt-money supply. And so the great bulk of the nation's money supply is this vast collection of loans, endlessly coming into existence for a short period of time, upon which interest must be paid of course, and then vanishing after doing their job of transferring that interest charge from a producing member of society to the businesses which control this money-creation machine, essentially imaginary money that people shuffle around between credit accounts, with every transaction thus undertaken additionally being skimmed a service charge, as every credit-dollar that is created is assessed interest, on and on and on and on, world without end. This is truly the golden goose laying an endless supply of golden eggs for those who control it, or the Midas touch for those who control this great power, as everything they touch turns to gold for them.

Well, respond those who still do not see the great problems with this, of course we need money to do the things we do in modern societies, buying things, getting paid for our work, etc, and it has to come from somewhere, so why is it so bad to have it coming from banks, which would seem to be a logical enough choice, considering they are in the 'money' business? And they seem to have been doing a pretty good job over the years, considering the prosperity of Canada, and other western countries ....

Actually, aside from the rather obvious evidence of the current world economic meltdown that something is seriously wrong with the system and maybe they haven't been doing such a good job at all (at least for those millions of people currently facing financial loss or ruin), this form of supplying our money is, very, very, very bad - so bad that the current financial meltdown, as I noted earlier, was a built-in, completely inevitable result. Kind of like playing tag on a small raft in the middle of the ocean - lots of laughs and thrills for awhile, but sooner or later it's going over. And then the laughs stop.

Let's look at this situation from a perspective you don't read in the mainstream Canadian media - media controlled, again of course, by the same people who control the banks, and are thus inclined to offer a certain perspective which is favorable to them, and disinclined to point out some things that might cast a somewhat more unfavorable light on their activities, even in this vast global meltdown we are currently experiencing, when casting a light on some truthful things might see a lot of people being charged with some very serious crimes rather than negotiating how big a bailout they are going to get.

Let's look at this situation from a perspective you don't read in the mainstream Canadian media - media controlled, again of course, by the same people who control the banks, and are thus inclined to offer a certain perspective which is favorable to them, and disinclined to point out some things that might cast a somewhat more unfavorable light on their activities, even in this vast global meltdown we are currently experiencing, when casting a light on some truthful things might see a lot of people being charged with some very serious crimes rather than negotiating how big a bailout they are going to get.

There are three major, interrelated reasons why letting commercial banks create virtually all of our money is so very bad (well, bad for 'we the people', obviously a pretty good game for the banks and their owners and 'investors' and paid flunkies who support them in government and media - but are we running our economy for the wellbeing of the small number of banks and their owner-investors and hangers-on, or the mass of people in our society as a whole? Again, this is not a trivial question - if you take a careful look around the last 30 years or so, with some thoughts gleaned from sources other than your mainstream Canadian media, the answer may not be the one you think obvious ...).

First - the interest: Interest may be a somewhat unpleasant but not unreasonable fact of life in some settings, for instance when a private citizen borrows already existing money from someone, as there is the idea of 'loss of use', or 'rental fee', that the lender is giving up something they could use productively to the extent the borrowed money diminishes the assets available to the lender, or even from a bank which pays interest on ('real' money) deposits and thus charges interest on loans, with its profit the difference. But it is very much another story when 'interest' is levied on the nation's entire money supply that we require to do the millions of daily transactions that are done in a modern country each day, and most especially when such 'interest' does not in any way compensate for any 'loss of use' suffered by the lender, since in the case of the bulk of the nation's money supply provided by the banks, they simply create it out of thin air by punching those numbers into their bank computers, making the 'interest' a 100% windfall payment to those commercial interests allowed to do the creating - and you can see that even in Canada, this is a pretty serious windfall, when the amount of such 'created from thin air' money is at least $3 trillion per year (this principle is somewhat muddied by the fact that loans get used to buy things, and the person receiving such money usually then deposits that money in a different bank, which gives that deposit account the superficial appearance of 'real' money, but the essential arguments I make here about the problems with allowing the nation's money supply to be loaned into existence are not diminished by this thaumaturgy). And remember also this is not even one-time interest in the great majority of cases, but year after year after year interest, compounding and compounding and compounding interest, on money created out of thin air. One might make an argument for the banks assessing a service charge of some sort on this created money, if we as a nation decided to allow our money to be supplied this way, but that is very much not what they do, and part of a different discussion.

It is kind of shocking when you think of this - our nation's money supply is basically imaginary. The banks create into existence through loans the electronic money that comprises the great bulk of our national 'money' supply, but that 'money' is not real, but exists only in your bank account, and the bank accounts of millions of other people and businesses, and is transferred between your bank account and others during the life of the loans that brought the imaginary money into existence. And the dangerous part is, the part that leads very inevitably to the kind of economical meltdown you see in the world today, is that with this system of money creation, you and all of us pay interest on those loans every year they are outstanding, which means we are paying interest on our very money supply, the lifeblood of our economy and modern lives, endlessly. Endlessly. Endlessly.

It is kind of shocking when you think of this - our nation's money supply is basically imaginary. The banks create into existence through loans the electronic money that comprises the great bulk of our national 'money' supply, but that 'money' is not real, but exists only in your bank account, and the bank accounts of millions of other people and businesses, and is transferred between your bank account and others during the life of the loans that brought the imaginary money into existence. And the dangerous part is, the part that leads very inevitably to the kind of economical meltdown you see in the world today, is that with this system of money creation, you and all of us pay interest on those loans every year they are outstanding, which means we are paying interest on our very money supply, the lifeblood of our economy and modern lives, endlessly. Endlessly. Endlessly.

So that is where 98%+ of your Canadian money supply comes from - banks punching numbers into computers and creating money-as-debt, upon which they then charge interest, month after month, year after year - money created for your new car, or a young couple's new house, or for wealthy speculators to go gambling on the stock market or in the foreign currency market, or for the Canadian government to go further into debt, all created by commercial banks looking to make a profit for their investors. And as we all well know, a very good profit they make indeed, from all that interest and service charges.

And although the people who want you to not think about this very much at all refer to this 'interest' as simply a 'business expense', as inevitable and natural and generally harmless as the night following the day, this is very much understating the actual seriousness of what is going on right under our very noses, day after day, month after month, year after year, decade after decade, as we pay interest on our very money supply, on the lifeblood of the nation, and pay and pay and pay and pay.

And although the windfall profits accruing to the commercial banks and their investors - windfall profits on at least $3 Trillion of created money each year in Canada alone - are certainly by themselves a good enough reason to examine this situation somewhat more closely than we ever have, there are much deeper and far more serious ramifications than the simple 'windfall' profits these commercial banks amass for the privileged few who are blessed with this great 'business' of creating and managing the nation's money supply.

Turn of the Screw the First: Systemic interest >> Systemic inflation: When you pay interest on virtually your entire money supply, you have built-in, systemic inflation - how can you not? Those who pretend to be the guardians of our economy, and teach us about it, and comment on it, point to oil shocks and workers demanding wage increases and house prices or food prices rising or similar things, and try to get you to believe that such things are the cause(s) of inflation, insofar as it can be explained at all and is not just some kind of natural disaster like a hurricane or ice storm that we can't really foresee or do much about except deal with after it strikes. However, although such things may be contributory, any of them taken alone are transient and not enough to cause ongoing national inflation, year after year, and they are also to a substantial extent responses to inflation rather than causes, and thus the argument is essentially tautological. But what is factual and straightforward and obvious to those who are able to think beyond the dogma fed to everyone by the economists and bankers et al is that when you have to pay interest on essentially your entire money supply each year, which is a big money supply and thus requires a lot of interest, year in and year out, in a system which is centered around businesses which must turn a profit each year or go broke, then as businesses try to keep up with the simple built-in cost of using the money they rely on to conduct their business dealings each year by raising prices rather than watching profits drop every year by the amount of interest the country pays on its money supply, inflation is built in and systemic.

And inflation, of course, impacts different sectors differently, but the impact is always heavier the further away from power you are, the lower in the social hierarchy - that is, the people at the mid and bottom levels of society are impacted the heaviest, as everything they use money for costs more, and more, and more year after year after year - but their incomes, whether government social support, or minimum/low wage jobs, or even unionized or non-unionized middle-class jobs (that is to say, the 85% or so of people who rely on 'jobs' for their income), never keep up. Professionals and top-level managers (and the politicians of course who are central in selling and maintaining this whole scam so are well looked after) always look after their incomes, and businesses raise prices as they wish - but the income of workers does not go up as *you* wish, and it takes much fighting to get raises that offset inflation even partially. Thus the reality everyone is aware of, for any middle/lower-class working family - whereas 30-40-50 years ago one person with a half-decent job could easily support a middle-class lifestyle and family, buy a house, save for retirement, put the kids through university, etc - in the last years of the 20th century and the opening decade of the 21st century, it takes two working adults to do these things for most families, and even with two people working most families are still falling further and further behind, as savings are far below what they were ~40 years ago (as a percent of income etc), and debt much higher. And this increasing pressure, this diminishment of security and savings and increasing debt, is all the inevitable result of the systemic inflation that results when we allow banks to create virtually all of our money supply, and charge interest on it, and there is no other place to get that interest year after year after year than through the inflationary process of creating more new money to cover the old debt, and that inflation eats into everyone's income as most of us cannot self-adjust our incomes to keep up.

(note - there are a number of references to '30-40 years ago' in the essay - this is because this is when the current economic crisis was birthed. After the great crash of 29, which was caused by exactly the same thing as the current meltdown/crisis (unregulated banks creating vastly more money than could be justified by the actual goods and services available in the real economy), governments throughout the western world, facing some very large numbers of very angry people looking for explanations and reassurances that such a disaster would happen no more, that their children would not suffer such a calamity, put in place various measures to control the banks and their money-creation power, to prevent another such meltdown. By the 1970s, however, with the prosperity enabled at least partly through such controls, the children now of the children of those days had forgotten about these controls altogether and what they had been established for, not without, of course, some considerable assistance from the corporations and banks, who were lobbying strongly and largely behind the scenes to have these controls removed, and in due time with little fuss they were. And the result was as inevitable as night following the day, or blindfolding your kid and putting him on his new bicycle and sending him out for a ride on the street. It is also relevant to consider another important contributory fact, that prior to the 70s, the western world was much more a 'cash-based' society - it is only in the years since then, through various technological advances, that the use of various forms of electronically-transferred 'credit' has rather quickly become so dominant in our daily activities, and the use of such credit as a money supply has become ever easier for commercial banks to create with little or no real oversight, and these things have never been properly understood or dealt with by our democratic governments - but the opportunities inherent therein for those controlling the electronic money have, of course, been much more quickly understood by the banks and the bank investors and their clever lawyers and economists, always alert to new ways to leverage their unique position of trust and power for profit, who have been, obviously, ready to take advantage of these new forms of electronic money and credit, and the lack of understanding of the average person, to the max.))

Turn of the Screw the Second: Imaginary money but real interest>>>> Another very important thing to understand, in terms of allowing commercial banks to create almost all of our money supply and charge interest for it, is that the banks create the money they lend - but they do not create the money for the interest they expect at payback time. This again you need to understand well, as it too is not a trivial esoteric point, but central to what is happening in terms of the current meltdown and the ongoing and accelerating transfer of the wealth of our society to a small elite at the top. Imagine, as a simple example, your local economy uses a million dollars, which is created by your friendly commercial banks - and then at the end of the year the loans come due, and they want that million repaid plus their 'service' charges - another 50 thousand. Where is that 50 thou coming from if they've only created the initial million? Well, two places, neither very attractive for 'we the people', although yet more gold from the goose for those creating the money. The first option for covering accumulated interest is simply to create that extra money each year as the whole 'loaned-into-existence' money supply is 'rolled over' into new loans, but more of them - essentially creating new money for no other reason than to pay interest on previously created/borrowed money. Any person with even a basic understanding of finances understands that borrowing new money simply to pay interest on old debts is a serious sign that your financial house is getting out of control - and yet here we have created an economy with this fatal flaw built right in, no way to get away from it, and it compounds every year, year after year after year!! We all know that interest is dangerous at the best of times, and compounding interest a truly radioactive problem once it starts doing its work unchecked. And then also, as will inevitably happen in the economy as a whole, many people will fail to find their little share of that required interest, and then they will lose property (collateral), and, again systemically mandated and quite inevitable, as the very rules of musical chairs mandate that someone is going to fall every time the music plays and then stops, over time as the interest compounds and the debts pile up, more and more real property will be turned over to those who create the money supply and demand interest, but do not create the interest but take the collateral when the interest cannot be found in the big financial game of musical 'find the interest!' chairs that never ends in an economy based on bank-created, interest-demanding debt 'money'.

Turn of the Screw the Third: Blind, highly destructive greed and selfishness driving the few who control the economy>> Inevitable Disaster for the many passengers: Although windfall profits for a privileged elite, built in inflation, and living within a system which is designed to turn real property over to banks to pay for imaginary money are certainly bad things, we have yet to pull back the curtain on the most important reason letting our money supply be created by commercial banks, with essentially no meaningful regulation, is a very bad thing for all of us, in both the long and short runs, and was the prime factor leading to the global financial meltdown.

Greed. Untrammelled greed - not as an expression in a book, but a fact. Greed allowed to control our money supply with no real oversight from 'our' elected governments - indeed, for much of the time this meltdown was developing, our government was actively helping those driven by greed by removing what few constraints remained on their activities from earlier days when at least a few responsible, sane adults in high places in government and even the business world understood that such freedom in those driven by greed could only lead to disaster.

Banks are run by real people, and the capitalists/'business'men who control our money and major businesses, including the banks, make no secret in the modern age of the fact that they are driven essentially by greed. Indeed, they glory in their greed, and many books have been written and speeches given by these people and their minions during this current period of capitalist ascendency in the world exalting this human trait. Greed is good!!! they proudly proclaim. But regardless of their enthusiastic support for this most rebarbative of the deadly sins, most normal, decent people accept that blind greed is not one of the better human characteristics, and really has no place in a civilized society, is very destructive when allowed to run amok in any community, and certainly has no place in the highest corridors of power in our nation, where those entrusted with such responsibility must look out for the wellbeing of all, not putting their own selfish interests above all. This repulsive trait might indeed lead to great wealth for those whose avarice is matched by a corresponding lack of ethics or morals, a willingness to bend or even break the laws that regulate the majority of honest and hardworking people in our society to acquire more money than their rivals, a willingness to act in secret to transfer great amounts of wealth from the bank accounts of others into their own, and brag lustily afterwards about their great cleverness, but such people are not normally held up as the type of person most normal people really want to invite over for Sunday dinner, or to have courting their daughter.

Prior to this age of greed we are now wallowing in, and facing disaster from, at any rate.

And yet, through some mysterious process, we have allowed a highly toxic and dishonest subset of these very people to place themselves in charge of our money supply, where the potential damage they can do is immense, as we are seeing now that the potential disaster is no longer potential but actually happening. And, as we saw in the great crash of 29, the savings and loan scandal, the dot-com bubble, the housing bubble which so recently imploded as the final straw that broke everything and led to the current global financial meltdown, and many other examples in both near and far history, letting these people create and control our money supply is, as I started out this short essay saying, a very, very, very bad idea. They obviously cannot control themselves, and to compound yet further their sins they lie readily, like an irresponsible, spoiled, wicked child, to conceal their true activities. The first priority of such people, driven by their own greed, is not a stable economy for all of us to live in but simply working their power to max their own takings from that system, and given the keys to the credit-producing machine create more and more 'credit' for the few who can access this money to speculate with, driving up prices in one area or another far beyond any sane assessment of their real worth, inflated bubbles which eventually, inevitably crash down in flames, destroying the lives of the millions of small people who got sucked into the growing maelstrom, but who do not have the protection to survive the crash as those who instigated it do.

The question must be asked - what possible good could come of having people who admittedly worship greed, who lie to conceal their activities, who corrupt the media and political process to enable those activities and avoid having them exposed, who have shown over and over again they cannot control themselves but will send the economy on a crazy roller coaster ride through the inevitable boom-bust-bubble-crash cycles time after time, be allowed to control our money supply?

And the only answer is, when the question is asked in a public, democratic forum - no good whatsoever, for We the People. As we are seeing so very obviously this year.

And yet, since the 70s, we have seen those who worship aggressive me-first Greed allowed once again to take control of our economy, with results perfectly predictable to those who could see beyond this quarter's profits, or had some understanding of history. Commercial banks are not in the business of creating a stable money supply for their community or country, they are in the business of making money, in every and any way, legal, quasi-legal and illegal, and with no regard for the human ethics or morality that guide most of us, for their 'investors' and owners - and what is good for an 'investor' and his drive to maximize profit is not what is good for the country as a whole - as we are seeing very obviously these days, what is good for the average GM or Citibank shareholder/investor is very much not what is good for the average American. Whatever size the pie is, however much it bubbles through their speculative price inflations, as long as the same 'investors' get to inflate it, then divide it up and get first choice of the select pieces during the bubble formation and leave themselves well-protected as it later inevitably implodes, as their greed indicates is the only approach to use in such an exercise, and their power gives them first dibs as it were, there is always less and less left to go around amongst 'we the people' after these cyclical asset inflations and following crashes of the real wealth we have produced through our lives of work. As we are seeing once again in 2008-9, as the corporate and bank executives jet off to their well-protected private south sea hideaways or gated Palm Springs communities or Mediterranean castles, after negotiating their final obscene grasp and suck at the national tit, as the financial world crumbles, whilst millions of average people lose jobs and savings and retirement plans etc etc etc.

And yet, since the 70s, we have seen those who worship aggressive me-first Greed allowed once again to take control of our economy, with results perfectly predictable to those who could see beyond this quarter's profits, or had some understanding of history. Commercial banks are not in the business of creating a stable money supply for their community or country, they are in the business of making money, in every and any way, legal, quasi-legal and illegal, and with no regard for the human ethics or morality that guide most of us, for their 'investors' and owners - and what is good for an 'investor' and his drive to maximize profit is not what is good for the country as a whole - as we are seeing very obviously these days, what is good for the average GM or Citibank shareholder/investor is very much not what is good for the average American. Whatever size the pie is, however much it bubbles through their speculative price inflations, as long as the same 'investors' get to inflate it, then divide it up and get first choice of the select pieces during the bubble formation and leave themselves well-protected as it later inevitably implodes, as their greed indicates is the only approach to use in such an exercise, and their power gives them first dibs as it were, there is always less and less left to go around amongst 'we the people' after these cyclical asset inflations and following crashes of the real wealth we have produced through our lives of work. As we are seeing once again in 2008-9, as the corporate and bank executives jet off to their well-protected private south sea hideaways or gated Palm Springs communities or Mediterranean castles, after negotiating their final obscene grasp and suck at the national tit, as the financial world crumbles, whilst millions of average people lose jobs and savings and retirement plans etc etc etc.

So our economy lies in ruins around us - and for one central reason, as I said at the first. We have allowed control of our money supply to be placed in avaricious hands, who have done very much as they might have been expected to do, if anyone outside the halls of power had of been paying attention. Brought us all to the edge of ruin.

So understanding the problem is one thing - but what is to be done?

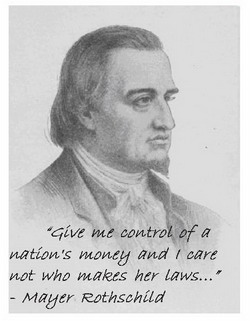

Simply making the problem clear makes at least the absolutely necessary first step of the solution equally obvious - taking this vast money-creation power out of private hands, and putting it where it belongs - that is to say, controlled democratically by 'we the people', with the objective of creating a stable money supply and economy for all of us, rather than leaving the creation of money in essentially private hands, whose primary interest is manipulating the money supply and anything else they can to maximise their own profits rather than looking after the public good. As we are seeing in 2008-9, and have many, many times in the past, a great deal of destruction can be done to 'the public weal' by out-of-control commercial banks, not only through huge windfall 'interest' payments on the entire debt-based, created-out-of-thin-air money supply leading to systemic inflation, but even more by creating vast amounts of speculative money, driving up prices and fuelling great bubbles which inevitably burst, spreading destruction throughout the entire economy, impacting most heavily millions of people who really had nothing to do with creating the bubbles, but surely suffer great consequences because of them. Really, it should be clear that no country can truly call itself a 'democracy' or the people therein 'sovereign', if this extremely important function, around which every modern economy and society revolves, is left in private hands - as the old saying has it, very truly, he who pays the piper calls the shots. Or, as one of the original bankers who began this entire bank-created-debt-money process is said to have said, "Give me control of a nation's currency, and I care not who writes her laws'. And in a very related way, our democracy is also very ill-served when people with the kind of vast wealth these banker/investors have also control our media in order to prevent people from understanding what is really happening with our money supply and economy, as they so obviously have been doing recently, presenting the entire world economic crisis as some kind of natural, unpredictable disaster, no blame to be assigned to anyone's feet, no discussion whatsoever of the things I talk about in this short essay, and how the money-creation power of these very banks can be tied very directly to this crisis.

Simply making the problem clear makes at least the absolutely necessary first step of the solution equally obvious - taking this vast money-creation power out of private hands, and putting it where it belongs - that is to say, controlled democratically by 'we the people', with the objective of creating a stable money supply and economy for all of us, rather than leaving the creation of money in essentially private hands, whose primary interest is manipulating the money supply and anything else they can to maximise their own profits rather than looking after the public good. As we are seeing in 2008-9, and have many, many times in the past, a great deal of destruction can be done to 'the public weal' by out-of-control commercial banks, not only through huge windfall 'interest' payments on the entire debt-based, created-out-of-thin-air money supply leading to systemic inflation, but even more by creating vast amounts of speculative money, driving up prices and fuelling great bubbles which inevitably burst, spreading destruction throughout the entire economy, impacting most heavily millions of people who really had nothing to do with creating the bubbles, but surely suffer great consequences because of them. Really, it should be clear that no country can truly call itself a 'democracy' or the people therein 'sovereign', if this extremely important function, around which every modern economy and society revolves, is left in private hands - as the old saying has it, very truly, he who pays the piper calls the shots. Or, as one of the original bankers who began this entire bank-created-debt-money process is said to have said, "Give me control of a nation's currency, and I care not who writes her laws'. And in a very related way, our democracy is also very ill-served when people with the kind of vast wealth these banker/investors have also control our media in order to prevent people from understanding what is really happening with our money supply and economy, as they so obviously have been doing recently, presenting the entire world economic crisis as some kind of natural, unpredictable disaster, no blame to be assigned to anyone's feet, no discussion whatsoever of the things I talk about in this short essay, and how the money-creation power of these very banks can be tied very directly to this crisis.

Of course, anyone would love to be able to print money, but most of us can't - why should any group, other than the democratically elected government of We the People, be able to do this? Did you ever have a discussion about this, and, with full awareness of all options and potential consequences, vote to have the national money supply created by a cartel of private businesses, with all the profit for the lucky few, and also all the power to create economic havoc at will by creating too much or too little money that that power contains? Of course not, and it is one of a handful of topics very deliberately and carefully kept out of the public debate, because just to raise the topic and examine it as I do here is to understand that the current system is very bad for We the People, and for Democracy as a whole, to allow a small group of people to have such great power.

The people who support bank-created debt money will immediately protest the idea of 'government created money' by throwing out another major myth that has been cultivated through the years when voices crying for money reform have arisen, as they do from time to time, that governments creating money is simply the worst thing possible, as governments are by definition terribly irresponsible and/or stupid, and venal politicians will just crank up the printing press, and with no understanding of the finer points of economic policy, they will create huge amounts of money to buy votes or something and thus create terrible inflation and destroy the economy. When this 'argument' is put on the table and the lights turned on it, however, like most arguments made by any fraud artist to convince marks to act against their own interests, it is quickly revealed as pretty much the reverse of the real situation.  A quick review of the history of the current world financial meltdown ought to be a solid enough refutation of the notion that commercial banks can responsibly control their money creation power, as during the last 30 years when the few regulations they faced were removed they have simply run wild, once again, in about as irresponsible a way as could be imagined, and created bubbles of various sorts, which inevitably crash with the loss of huge amounts of money for average investors (with, of course, the attendant expectations that those 'investors', as taxpayers, will be hit twice, as they must also contribute yet more money through their taxes to the bailouts these banks then demand). As they did during the 20s leading to the great crash of 29, as they did during the dot-com bubble a few years ago or the recent subprime mortgage bubble that catalysed the current meltdown, and anyone familiar with financial history can quickly put together a long list of such things. In rather sharp contrast, in terms of government-controlled-at-least-to-some-extent money, we have the period following the 29 crash, when, to control the excesses of the banks that led to that crash, the governments most impacted by this crash, including in Canada, put some serious controls on bank-created money. The years of coming-out of the depression and then WWII are difficult to analyse, but it is clear that following WWII, from the late 40s until the early 70s, when the western governments kept a much tighter rein on bank-created money and on the economy in general, and used their own government powers to create at least most of their own needs via central banks, was a period during which the economy was much more stable. But then during the 70s people (with the help, of course, of the corporate-controlled media) seemed to forget the lessons of the 29 crash, and corporate-banking entities, always looking for ways to maximise their takings from the prosperous western economies, lobbied our governments to again relax and even remove the controls on bank created debt-money, and, with the increasing availability of electronic credit-money unregulated also by the governments, thus began the current bubble that is now crashing down all over the world, destroying the lives and savings of millions of 'ordinary' people who had nothing to do with creating the crisis, as in the last great crash of 29, but are most assuredly expected to pay the price with all the great bailouts now being implemented, which are little more than blatant thefts by the highly unrepentant banks and their government servants from future generations who will be expected to pay all of these government debts that are being incurred, through the demonstrably insane process of using the very process (bank-created debt money) as a 'cure' for the crash caused by that very process. A quick review of the history of the current world financial meltdown ought to be a solid enough refutation of the notion that commercial banks can responsibly control their money creation power, as during the last 30 years when the few regulations they faced were removed they have simply run wild, once again, in about as irresponsible a way as could be imagined, and created bubbles of various sorts, which inevitably crash with the loss of huge amounts of money for average investors (with, of course, the attendant expectations that those 'investors', as taxpayers, will be hit twice, as they must also contribute yet more money through their taxes to the bailouts these banks then demand). As they did during the 20s leading to the great crash of 29, as they did during the dot-com bubble a few years ago or the recent subprime mortgage bubble that catalysed the current meltdown, and anyone familiar with financial history can quickly put together a long list of such things. In rather sharp contrast, in terms of government-controlled-at-least-to-some-extent money, we have the period following the 29 crash, when, to control the excesses of the banks that led to that crash, the governments most impacted by this crash, including in Canada, put some serious controls on bank-created money. The years of coming-out of the depression and then WWII are difficult to analyse, but it is clear that following WWII, from the late 40s until the early 70s, when the western governments kept a much tighter rein on bank-created money and on the economy in general, and used their own government powers to create at least most of their own needs via central banks, was a period during which the economy was much more stable. But then during the 70s people (with the help, of course, of the corporate-controlled media) seemed to forget the lessons of the 29 crash, and corporate-banking entities, always looking for ways to maximise their takings from the prosperous western economies, lobbied our governments to again relax and even remove the controls on bank created debt-money, and, with the increasing availability of electronic credit-money unregulated also by the governments, thus began the current bubble that is now crashing down all over the world, destroying the lives and savings of millions of 'ordinary' people who had nothing to do with creating the crisis, as in the last great crash of 29, but are most assuredly expected to pay the price with all the great bailouts now being implemented, which are little more than blatant thefts by the highly unrepentant banks and their government servants from future generations who will be expected to pay all of these government debts that are being incurred, through the demonstrably insane process of using the very process (bank-created debt money) as a 'cure' for the crash caused by that very process.

It is a subject about which much disinformation and falsehoods often approaching simple outright lies have been spread around by those with large interests and untrammeled power to protect and maintain, with ample willing assistance from those in media and government who serve this power, but when considering all the propaganda spread around by proponents of bank-created debt money vs government controlled money, you should at least consider one question: as a voter in a true democracy, participating in discussions and decisions about how to provide your money supply, and how much money to have in circulation, understanding the ramifications described above of a highly unregulated, mostly-commercial-bank-created debt money supply - would you vote to allow private banks to control the money, driven by people who extol the virtues of greed, with its windfall profits and debilitating systemic inflation, and with no supervision create huge amounts of debt-based speculative money to create a casino economy where a few might win big but millions of small people would suffer, as the unregulated banks have done over the last 30 years and any other time in history they have had such a golden opportunity for self-enrichment - or would you at least be interested in checking out some democratically controlled alternatives, which promise a considerably more stable money supply and thus more secure lives for average people? Do you think the capitalist 'boom-bubble-bust' 'business' cycle is a good thing because sometimes a few people get really rich, although many more people lose everything - or would you prefer a more stable economy through which we all were secure in both present and future, no great exuberant bubbles for the few to get vastly wealthy on, but on the other hand no serious downturns or recessions or even depressions which deprive millions of their jobs and savings?

Again, to ask the question "What is to be done?!?" is to answer it, which is why you will never see this discussed, in this way, in your 'free and responsible' Canadian mainstream media, who serve first and primarily their investor-owners - the same people who control the banks and thus the money creation power, and which they do not really want the Canadian people understanding, for quite obvious reasons. The reason nobody seems to be able to do anything is simply because the only real solution - democratic control of the money supply, exposure of this entire massive fraud, declaring most of the current 'debts' for the fraudulent acquisitions they are and thus of no legal force, and putting a whole lot of people on public trial and then jailing them for the rest of their lives - is something that is never going to happen, as long as they sit in the seats of power - what major criminal will admit their guilt, give back the loot, and put themselves on trial and in jail? It isn't going to happen - they fought for centuries for this power, and they will not give it up by themselves.

But to have a sane economic policy requires something even more fundamental ....

So the plot thickens somewhat, as we now see that the first necessity, as we look for a way out of the current world financial meltdown, is simply open democratic decision making, which is currently not the way the money supply is organised, or the rest of the country, for that matter. If you think your country is a 'democracy', then you are as mistaken about that as you have been about understanding anything about your money supply - think of such things as most Canadians opposing 'free trade' when Mulroney signed this major treaty which put corporations in the driver's seat of our government, or NAFTA when Chretien signed that one, or most Canadians opposing the Afghanistan invasion, or most Canadians not feeling pot smokers or growers should continually be harassed as criminals, etc and etc - we are, indeed, a 'majority-rules democracy' much more in theory than in fact, which has been very central to this entire monetary supply scam being enabled and foisted upon us, and us knowing nothing of it through our somewhat less than truthful media, owned by the same people who control the banks - and before we can correct the economic problem, we will find we must deal with the democracy problem first.

We obviously cannot have a national meeting several times a year negotiating details about the money supply, and it is not necessary any more than we exercise minute-by-minute supervision of any public servant or body - but we should be able to formulate, after open and appropriate discussion informed by people knowledgable in a money supply created and controlled by 'we the people' for our benefit rather than 'they the bankers' for theirs, a certain framework within which those we elect or otherwise hire as **employees** of We the People to manage the daily business of overseeing this all-important national function operate, and about which they issue regular, full reports and whose decisions are subject to our approval so we can keep a fairly close eye on things if any of them decide they would rather work secretively for the bankers and against us, as they all seem to be doing now.

The Fix

But let us assume for a brief fantasy that we had a democratic revolution, without the current rulers destroying us dog-in-the-manger fashion before we manage to take over rather than relinquishing their power (this will be our major problem, I think), and had to solve this problem. What steps could be taken?

The current proposed fixes, designed to maintain the status quo, are demonstrably insane - to fix a meltdown caused by the banks creating too much money, our governments are proposing that the banks create yet more huge amounts of money, which the governments will then borrow and inject into the economy, leaving our children to deal with the debts thus occurred. Robin Hood lies on the edge of death because the barber has bled him too much - so the solution? Call the doctor to bleed him some more!! It was treachery then - and I would suggest what we are seeing today is equally treacherous.

In a sane country run by sane people, first of course we would have to declare a moratorium on all current major bank debt as it was investigated, as it is obvious that some very large percentage of it is fraudulent in one way or another (or several together), and thus of no legal force, in a sovereign democracy run by 'we the people' rather than the bankers. Democracies do not allow fraudulent debts to be created to control their citizens, that is the territory of dictatorships or thoroughly corrupt regimes. This would very obviously include the notion of a government creating a huge debt through borrowing bank-created money rather than creating debt-free money themselves, and then requiring the children of the current citizens (or the children of the children) to assume responsibility for such debts (check out a principle called Odious Debts). We would also be initiating some in-depth investigations to determine how deep and how far back this fraudulent activity stretched - it is quite obvious on the surface, for instance, that these activities go back at least to the 1970s, and thus most of the entire Canadian national debt (and the corresponding provincial and major municipal debts) were levied on the Canadian people through fraudulent practices, and thus are not legally binding - which then means that an attempt must at least be made to recover the couple of trillion dollars that have been paid on those debts as 'service charges'. There is no civilized country in the world in which criminals are legally allowed to profit from their crimes once the crimes are uncovered, and this principle should be followed here, as well. And of course those who signed the papers and did the work to get those debts in place, and the golden interest goose laying those golden service charge eggs year after year after year, should also be investigated - the claim of innocence and/or stupidity is going to be pretty hard to substantiate at those levels of government and the financial world, and the prima facie case for blatant fraud is pretty much overwhelming once the basic principles of where our money comes from, and the choices available, are understood - if We the People controlled the legal and police systems, and media, rather than the same people who have perpetrated this fraud upon us, they would have been called before a court of true justice long ago, you have to think.

And then, once the current rot is thoroughly exposed and steps are underway to excise it, to establish a solid economy, and get people working and economic gears turning again, the Bank of Canada must take over what it should have been doing all along - control of the money supply of the nation. It is probable that the basic system we now have, with a certain percentage of 'hard' money for daily small transactions supplemented by a much larger store of 'electronic' money circulating much as it does now primarily through debit and credit cards or just electronic paperless transactions via the internet, will remain in place - the major difference will be that the great bulk of our money will no longer require interest to be paid on it every year, which will be of enormous benefit to us all, via both reduced obligations in general, and finally slaying once and for all the cancer of systemic inflation year after year that has so diminished the economic wellbeing of most people over the last 30 years.

With democratic control of the money supply, there will be ample money available for investment in any real business, or as loans for productive activity. These decisions will be made democratically, of course, and I won't be the dictator, but I rather suspect that, for instance, if a young couple wants to build a house, or a group of people want to open a small business, there will be money available from a central bank, but if a wannabe billionaire wants the bank to create a billion so he can go currency attacking, or a group of speculators decide to create a stock bubble or housing bubble or any other bubble using borrowed money, they will be told that gambling with one's own money is legal, of course (if not encouraged), but the Canadian government is not in the business of abetting such activity. And such loans will be made at either greatly lower interest rates than are now required (we will not need to account for inflation, nor feed the ROIs of avaricious 'investors'), or perhaps even only a small yearly service charge - there is no need for 'we the people' to require profit on the furnishing of our money supply to ourselves - this will benefit everyone.

Several things would follow from such a major shift in our policy, all of them highly advantageous for We the People, although perhaps less so for those who are currently extracting huge takings from the current system. For instance, imagine if we turn the above money supply figures around - that is, currently about 2% of our money is 'real' money, and 98% is debt, which is constantly retired and re-created and thus requires interest on it every year. But what if the great bulk of our money supply was 'hard money', not being disappeared and recreated constantly and thus not requiring that endless stream of interest which is, as I have shown, so destructive in so many ways?

Nothing but good could come of this, at least for the great majority of 'We the People'.

First and most importantly, this 'boom-bust-bubble-crash' cycle that destroys so much of the wealth of the ordinary people of the country would become history. Booms and bubbles happen when banks create too much money, primarily the last few years as we have seen, as they did in the years leading to the 29 crash, for speculation, which adds nothing to the real economy except bad things such as destabilization.

Likewise, the current 'recession/depression' we are experiencing, which happens when the banks reverse their on-steroids money-creation-for-speculative-asset-inflation purposes and slow down the money creation to levels too low for businesses to continue operating, would also stop, as the 'hard money' residing in our community and personal accounts could not be destroyed so easily, and the money we had as a nation, based on our work and real wealth creation, residing in whatever form, would still be there for businesses to access as they needed - and such access guided by standards set by the community for purposes of a stable economy with sustainable growth and real investment rather than money-creation with the primary focus of maximizing bank profits through various kinds of speculation, which is to say in a democratically-controlled system we would see all the access needed for productive investment but not speculative gambling (which is essentially the reverse of the current banking policies which led to the current meltdown).

Also, the systemic inflation that is so debilitating to average people over the years would also stop being a problem, as when we no longer needed to pay interest on our money supply, there would be no inbuilt expense requiring businesses to increase their prices every year or lose money, leading to systemic inflation and workers' incomes falling more and more behind. (There is a small 'natural' inflation that follows as society in general grows and progresses, from advances in technology, increasingly complicated goods and services requiring more inputs as part of a growing population, and related things, but with such 'natural' inflation, carefully monitored in a democratic setting, both prices and wages will increase at more or less the same rate, leading to neither windfall profits for a few nor lagging wages for the many, nor the kind of instability and hardships for those on the receiving end the kind of systemic, greed-based inflation we are used to is associated with.)

We could forget the national debt that has drained at least two trillion dollars from our collective coffers the last 30 years in 'service charges' on the bank-created debt money, thus making our governments much more able to provide the programs and services most Canadians think they should have, and more, such as a modern health care service available to all with no waiting lines, drug provision, providing free university education for our young people, allowing them to start lives after graduation without facing a decade or more of paying back huge student loans, ballooned to ridiculous levels through additional compounded interest, and etc and etc.

And imagine a bit further ahead - imagine a society where a substantial portion of everything the average worker produces through his or her work is not drained off one way or another, either through interest and inflation year after year, or through the capitalist appropriation of 'surplus value' which controls modern society, but which would lessen and eventually stop altogether if banks of We the People supported communities and people rather than corporations - we could all work much, much less, but have much, much more, as the surplus value we produced in our modern society was saved for our future use, rather than being skimmed off at the end of every work day to enrich the bankers and small elite who currently control our society and work. Environmental destruction, a major issue in the modern world, would immediately have some serious brakes put on it, as so much of what we call modern 'work' is performed simply to create 'value' for the capitalists to exploit to become rich - if a good stable society was our goal, rather than creating a small class of obscenely wealthy overlords, we would no longer need to mine our environment to the very edge of destruction as we are currently doing.

But those are all dreams for another day - first comes the understanding of the money supply sting that has been ongoing for centuries, and stopping it, and creating a true Democracy in our country, with meaningful votes for people rather than dollars, which should be a good day's work for one generation. Let our children have the rewards of peace and freedom and security through a stable economic system, rather than the chains of eternal debt the current rulers are trying to place upon them.

But those are all dreams for another day - first comes the understanding of the money supply sting that has been ongoing for centuries, and stopping it, and creating a true Democracy in our country, with meaningful votes for people rather than dollars, which should be a good day's work for one generation. Let our children have the rewards of peace and freedom and security through a stable economic system, rather than the chains of eternal debt the current rulers are trying to place upon them.

Knowledge is power. Now you have it - use it.

Click on the poster to download a printable and copyable PDF

of this essay to pass around and share with others...

REFS

You ought to google around and verify things yourself, but here are a few places to start -

The Money Masters (google if this link doesn't work, things have a way of changing) - an excellent history of the struggle between the bankers and those who preferred democratic control of the world's money supply. We know who is winning, so far ....

Money as Debt - the original film by a guy called Paul Grignon, explains it all clearly. Also available on youtube if you don't want to buy it. Google.

A few books with more info (there are many more, but these are a starting place):

- Web of Debt by Ellen Hodgson Brown

- Grip of Death by Michael Rowbothom - not online, but worth getting your library to order for a very good history of banking and all this money-creation stuff - he has a very good short article introducing it all at Prosperity UK, where you will also find a lot of other good info

- The Lost Science of Money, by Stephen Zarlenga of the American Monetary Institute - - I haven't read this, but it sounds very good

- James Robertson and the New Economics Foundation - - many books and articles

- The Two Faces of Money - again, I haven't read this, but the web page has quite a lot of good info (quotes, etc), and the book seems to cover the territory well, without the libertarian 'let the market rule!!' snake in the grass you have to watch for with stuff like this ...

- - and an excellent recent article from a good site called Information Clearing House - A New Monetary System by a guy I haven't heard of but who obviously knows his stuff, Nikki Alexander

- -- Just google Monetary Reform, and you'll get lots of interesting reading

Footnotes

Footnote 1: There will be protests from some that of course there are controls! - but quite obviously the current world meltdown, caused by vastly more money floating around speculating on everything and driving up prices to levels far above what can be justified by any sane economic standards, as has happened regularly the last 30 years with the 87 crash, the dot-com crash, the savings and loan stuff, the Canadian bank bailouts of the early 80s and 90s, the housing bubble, and etc etc, which were/are ALL the direct result of out-of-control bank-created debt money, is about all the proof anyone would need that any such 'controls' are far more theoretical than actual.back to where you were

Footnote 2: War and world poverty and environmental destruction are very much related to bank-created debt money and the people who control it all for their own purposes, as well as the obvious money-related problems such as governments claiming poverty so they have no money for a decent health care system or to do something about huge student debt, etc and etc - I can't cover everything in one short essay, but it may be something rewarding to think on once you finish here ... back to where you were

Footnote 3: An exact 'authorised' figure is hard to find for Canadian 'legal tender' in circulation (scamsters avoid verifiable stuff like the plague, as you no doubt know), but these two non-conspiracy-theory sources give figures indicating the same ballpark - Taxtips (question 1, about half way through - 40 billion) and Bank of Canada Fact Sheets - Seigniorage Revenue (last para, 35 billion 'in recent years' - prior to 2001, and we've come quite a ways since then in every way - remember, I'm only trying to get you in the ballpark here, not do an academic study of any kind)

Business debt - - Canadian business debts rise, Toronto Star, Dec 05/08

Consumer debt - Where Does the Money Go: The Increasing Reliance on Household Debt in Canada (from the CGA, Certified General Accountants of Canada, probably reliable non-conspiracy theory data)

Government debts - anyone reading this will be aware that the federal debt is something under $500 billion now, but was around $550 billion for many years, and the debts of the provincial governments and major municipalities - all of which can and should have been assumed by the Bank of Canada more or less interest free but were part of all of this banketeering scam - amount to at least as much. Go google.back to where you were

If you thought this short essay useful, you'd probably enjoy a read of Green Island, a story of a modern social democracy where We the People have finally displaced the bankers from our government, and things work much better. We follow a couple of old Utopians around Green Island as they see how things are done in a truly democratic society - and then follow the excitement as, predictably, the bankers are not about to sit idly by and allow the work of centuries to be undone by a band of hippies, and attempt a regime change with their military arm, the US army. This regime change gets a bit of a shock, however. Green Island too has something a little harder under the green glove.

And don't miss Dave's warning about what is happening to our society - They're Building a Box - and You're In It - Dave's take on what is happening here, Mr Jones.

And don't miss Dave's warning about what is happening to our society - They're Building a Box - and You're In It - Dave's take on what is happening here, Mr Jones.

|